How UAEFIU shapes Dubai real estate compliance

TL;DR:

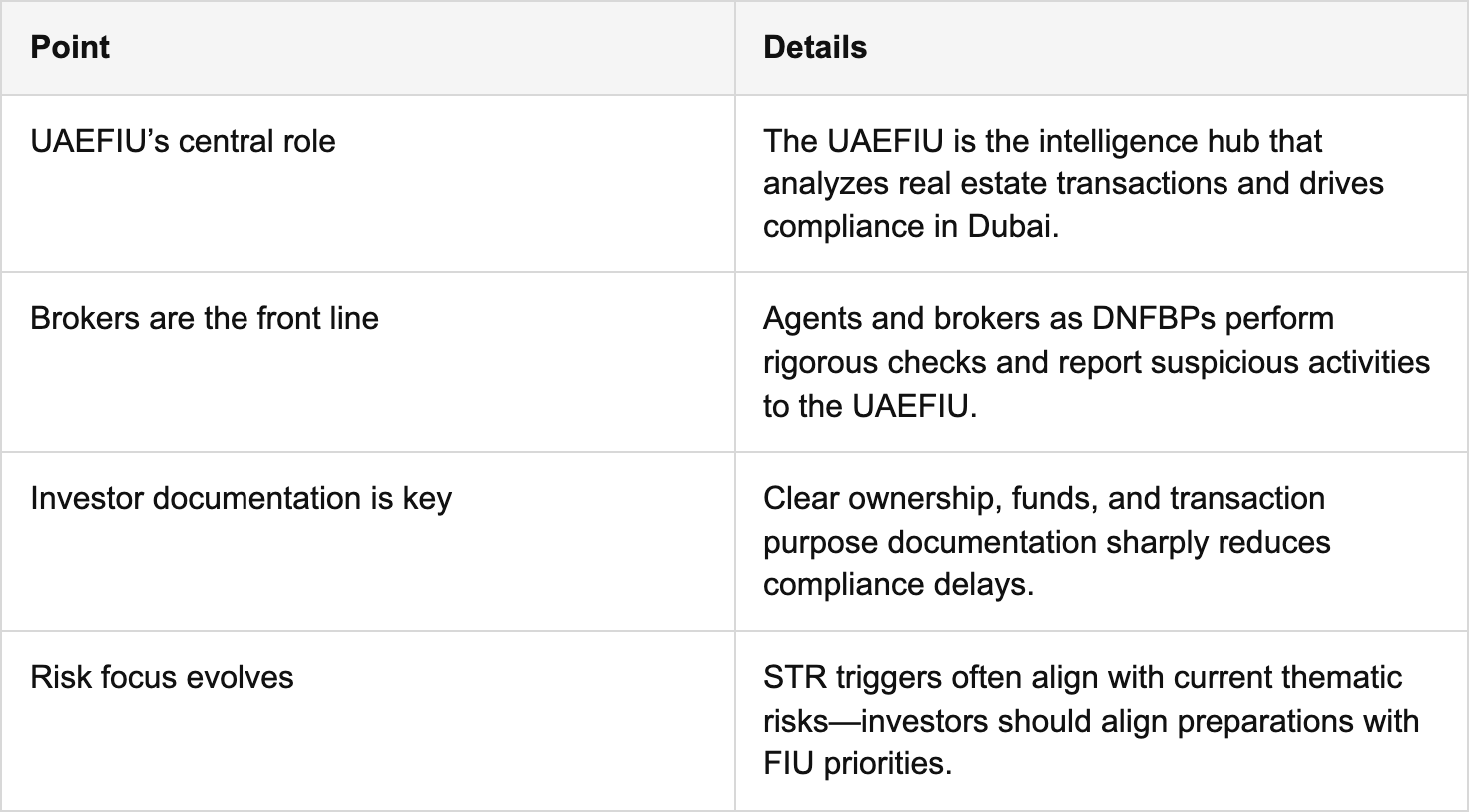

- Regulatory oversight by the UAEFIU extends beyond banks, scrutinizing Dubai property transactions for suspicious activity. Real estate brokers and agents are legally required to file STRs and SARs, which can delay deals despite investor compliance. Proactive documentation and understanding current AML risks help investors navigate the evolving intelligence-driven enforcement landscape effectively.

Luxury property deals in Dubai can be flagged for regulatory review even when every party at the table believes the transaction is fully compliant. That counterintuitive reality stems from the intelligence-driven oversight of the UAE Financial Intelligence Unit (UAEFIU), a body that operates well beyond the banking sector. For high-net-worth individuals and international investors, understanding this layer of scrutiny is not a legal formality. It is a strategic requirement that directly affects deal timelines, clearance outcomes, and long-term investment security in one of the world’s most dynamic property markets.

Table of Contents

- What is the UAEFIU and why does it matter in real estate?

- How real estate brokers and agents fit into the UAEFIU’s process

- From transaction to report: How property deals reach the UAEFIU

- Investor strategies: Reducing the risk of transactions being flagged

- Why most investors overlook the FIU’s real-world influence, and what actually works

- Get expert guidance for seamless Dubai real estate transactions

- Frequently asked questions

Key Takeaways

What is the UAEFIU and why does it matter in real estate?

The UAEFIU is the national center for receipt and analysis of suspicious transaction and activity reports across the UAE. Its mandate extends far beyond commercial banks and exchange houses. Under UAE anti-money laundering (AML) legislation, real estate is classified as a sector of designated non-financial businesses and professions (DNFBPs), meaning property transactions fall squarely within the UAEFIU’s intelligence and enforcement scope.

This classification is significant. It means that brokers, agents, developers, and related service providers are all bound by the same core reporting obligations as financial institutions. The UAEFIU acts as the central hub connecting data streams from the property sector to law enforcement, regulatory authorities, and international financial intelligence networks. When a suspicious transaction report (STR) or suspicious activity report (SAR) is filed from within the real estate sector, it does not sit in a silo. It feeds directly into an intelligence picture that informs enforcement priorities across the UAE.

The UAEFIU’s reach into real estate is also shaped by DLD and real estate oversight through the Dubai Land Department, which cooperates with financial intelligence bodies to maintain transactional integrity across the emirate. This coordination means that data from property registrations, title transfers, and developer sales can all intersect with AML reviews at multiple points.

Key functions of the UAEFIU relevant to property investors include:

- Receiving STRs and SARs from all DNFBPs, including real estate agencies

- Analyzing transaction patterns and producing sector-specific thematic reports

- Disseminating intelligence to the Public Prosecution and relevant authorities

- Tracking typologies such as beneficial ownership opacity and high-value cash movements

- Feeding intelligence to international counterparts under the Egmont Group framework

The scale of this mandate means that property investors who treat AML compliance as a back-office banking formality are operating with a significant blind spot.

How real estate brokers and agents fit into the UAEFIU’s process

Now that you understand why the FIU exists, it is crucial to know how brokers and agents function as its frontline in the real estate sector.

Under UAE law, real estate brokers and agents are DNFBPs with defined AML and counter-financing of terrorism (CFT) reporting obligations to the UAEFIU. This is not optional compliance. It is a legal duty that carries significant liability for any broker or agency that fails to act on it. For investors, this reframes what a broker actually does during a transaction. Their role is simultaneously commercial and regulatory.

The compliance workflow a professionally licensed broker follows typically includes the steps below:

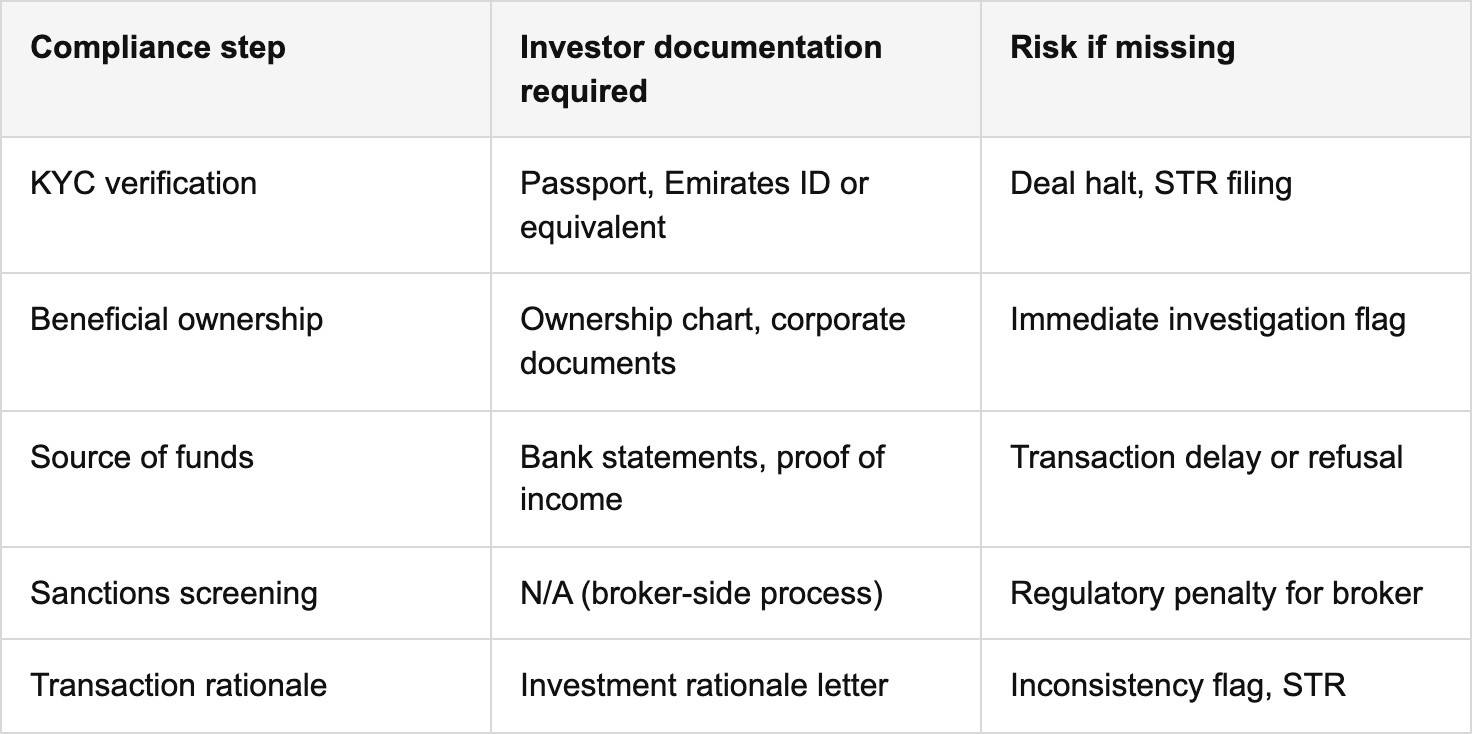

- Know Your Customer (KYC) verification: Collecting government-issued identification, proof of address, and confirming that the identity presented matches public records and sanctions databases.

- Beneficial ownership check: Identifying who ultimately controls or benefits from the entity purchasing the property, especially when the buyer is a corporate structure, trust, or special purpose vehicle.

- Sanctions and politically exposed persons (PEP) screening: Cross-referencing the buyer against UAE Central Bank, OFAC, UN, and EU sanctions lists before proceeding with the transaction.

- Source of funds validation: Requesting documentary evidence that the funds used for the purchase originate from legitimate, traceable economic activity.

- Transaction rationale assessment: Evaluating whether the deal makes logical economic sense given the buyer’s declared profile, occupation, and financial history.

- Ongoing monitoring: Reviewing any material changes to the buyer’s profile or the transaction structure throughout the deal lifecycle.

If inconsistencies arise at any of these stages, the broker has a mandatory obligation to file an STR or SAR via the goAML portal, which routes directly to the UAEFIU. Importantly, the broker cannot tip off the investor that a report has been filed. That tipping-off prohibition is itself a statutory requirement.

Pro Tip: Before you engage any broker for a high-value acquisition, request their AML compliance framework documentation. A reputable, brokerage with strong compliance requirements will have this structured and ready to share. It tells you they are equipped to handle the regulatory weight of your transaction professionally.

Understanding what drives high-net-worth client engagement in compliance-sensitive transactions is equally useful, since it mirrors exactly what experienced brokers look for when managing large portfolio acquisitions.

From transaction to report: How property deals reach the UAEFIU

With brokers and agents as the first line, here is how transactions flow or get flagged in the regulatory machinery.

The UAEFIU’s thematic analysis has noted an increase in reported fraud and suspicious activity originating from the real estate sector, directly shaping enforcement priorities. This means that the type of deal you bring to the table, its structure, and its documentation quality will be assessed against an evolving intelligence backdrop, not a static checklist from five years ago.

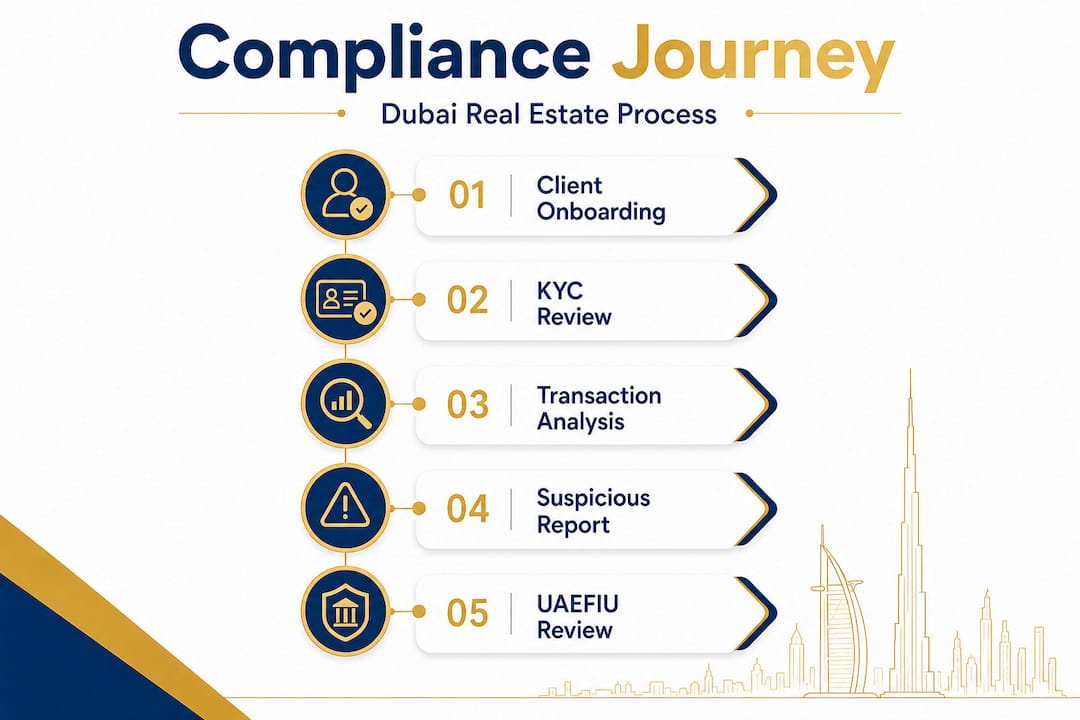

Here is the sequence a high-value property transaction follows through this system:

- Offer accepted and KYC initiated: The broker collects your documentation and begins screening. Any mismatch between declared identity and financial profile triggers internal review at this stage.

- Documentation review: Supporting documents are assessed for consistency. A passport from a higher-risk jurisdiction paired with funds routed through multiple intermediary accounts, for example, creates an immediate friction point.

- Broker risk assessment: The broker determines whether the transaction matches your declared economic profile. A first-time buyer purchasing a AED 25 million penthouse with an employment income background will attract more scrutiny than an established institutional investor with a documented acquisition history.

- goAML portal filing (if triggered): If the broker identifies sufficient grounds for concern, they file an STR or SAR. This is a unilateral step. The investor is not informed.

- UAEFIU analysis and dissemination: The unit reviews the report, cross-references it with existing intelligence, and may disseminate findings to enforcement authorities for further action.

- Transaction clearance or investigation: Most compliant deals proceed. However, deals flagged during STR review may be subject to delayed clearance, requests for additional documentation, or formal investigation.

“The most common cause of transaction delays is not insufficient funds or legal complexity. It is incomplete documentation at the beneficial ownership stage, which triggers a precautionary STR even when no actual wrongdoing is present.”

As part of your due diligence process, following a structured due diligence checklist ensures your documentation aligns with what the compliance workflow demands at every step. Understanding the notary’s role in property transactions also matters here, particularly when verifying the authenticity of sources of funds documentation submitted during the deal.

Consider this scenario: An international investor purchases a luxury villa in a prime freehold zone. The property is structurally sound, the price is fair, and the buyer has sufficient funds. However, the purchase is routed through a holding company registered in a jurisdiction with a limited public ownership registry, and the investor does not immediately provide a clear rationale for using that structure. The broker, fulfilling their statutory duty, files an STR. The transaction stalls for several weeks while documentation is reviewed. No wrongdoing is found, but the delay affects refinancing timelines and costs the investor materially. This outcome was entirely preventable with better documentation preparation.

Investor strategies: Reducing the risk of transactions being flagged

Once you understand how flags are raised, you can take practical measures to ensure transactions proceed smoothly.

The core principle here is anticipation, not reaction. Documentation planning reduces filings triggered by inconsistency with investor profile or absence of clear economic rationale. Equally, risk frameworks should align to current UAEFIU priorities and thematic intelligence trends, not only to the generic AML checklists that were standard practice a decade ago.

Here are the most effective strategies for investors navigating this environment:

- Prepare a source of funds dossier before you begin. This should include bank statements covering the last 12 to 24 months, tax filings or income declarations where applicable, and a written narrative connecting your wealth history to the purchase funds. The more clearly this tells a coherent story, the less friction you encounter.

- Simplify ownership structures where possible. If a corporate structure is necessary for estate planning or tax efficiency reasons, document it thoroughly. Provide ownership charts, company formation documents, and ultimate beneficial owner declarations upfront, rather than in response to a request.

- Prepare a transaction rationale letter. A one to two page document explaining why you are purchasing this specific property, at this price, through this structure, removes one of the most common triggers for precautionary STRs. It sounds simple. Most investors do not do it.

- Align your documentation to current UAEFIU risk typologies. The UAEFIU’s annual reporting identifies specific risk trends, such as fraud typologies, misuse of legal persons, and cross-border fund layering. Investors whose profiles touch any of these patterns should be proactive about addressing them.

- Support your broker’s compliance workflow actively. Respond to document requests promptly, provide certified translations where required, and avoid restructuring the transaction mid-process without a clear explanation.

Pro Tip: Review the latest UAEFIU annual report before closing a significant transaction. It identifies the sector-specific risk typologies that enforcement authorities are currently prioritizing. Aligning your investor rights and risk management approach to these current signals is far more effective than relying on standard AML guidance alone. Seasoned investors using advanced property acquisition strategies already build this intelligence review into their pre-transaction preparation.

Why most investors overlook the FIU’s real-world influence, and what actually works

Most compliance guides focus on the visible actors: the bank, the notary, the Dubai Land Department. Investors prepare for bank-level AML reviews, gather their documents, and consider the job done. The reality is that the most consequential compliance decisions in Dubai’s property market happen at the broker and agent level, long before a bank sees any transaction documentation.

This matters because the UAEFIU’s intelligence function is not passive. It is thematic, adaptive, and informed by cross-sector data. A deal that would have passed standard AML review two years ago may attract additional scrutiny today if its structure matches a current risk typology, even if nothing about the individual investor has changed. The system evolves. Most investor preparation does not.

The practical implication is this: box-ticking compliance is insufficient. You can produce every document on the standard list and still have a transaction delayed because your deal pattern matches an emerging fraud typology that the UAEFIU flagged last quarter. The investors who navigate this environment most smoothly are those who combine full documentary transparency with an active awareness of sector intelligence trends.

Experienced local brokers who operate at the high end of the market already build this awareness into their practice. They know what the UAEFIU has been focused on recently, and they help their clients prepare accordingly. Partnering with such professionals is not merely convenient. It is a strategic advantage that directly affects deal certainty and timeline. Avoiding the most common investor mistakes in Dubai real estate often comes down to choosing advisors who understand the compliance landscape at this level of depth.

The investors who struggle are typically those who treat the regulatory process as an administrative burden to be managed minimally. The investors who succeed treat it as part of the deal architecture, building compliance readiness into their preparation from the outset.

Get expert guidance for seamless Dubai real estate transactions

Navigating the UAEFIU’s compliance landscape requires more than standard AML preparation. It demands a partner who understands the intelligence-driven nature of regulatory oversight in Dubai’s property market and can help you structure your transaction accordingly.

At anthonyjosephaj.com, we work directly with high-net-worth individuals and international investors to provide the depth of due diligence, compliance preparation, and deal structuring support that today’s regulatory environment demands. From source of funds documentation to beneficial ownership disclosure strategy, our approach is built around protecting your investment timeline and ensuring your transaction clears the compliance chain without unnecessary friction. Reach out today to access one-on-one expert guidance tailored to your specific investment profile and objectives.

Frequently asked questions

Are all real estate transactions in Dubai reported to the UAEFIU?

No. Only transactions that raise red flags during the broker’s AML review process are reported, and STRs and SARs are triggered by suspicious activity, not by routine compliance checks on standard deals.

What are the main red flags brokers watch for when dealing with high-value property deals?

Common triggers include unclear source of funds, complex or opaque ownership structures, and transactions that lack a logical economic rationale, with ownership opacity and missing transaction rationale consistently listed as leading STR triggers.

What practical steps can investors take to minimize regulatory issues?

Prepare a comprehensive source of funds dossier, document your ownership structure clearly, and provide a written transaction rationale, since documentation planning actively reduces filings based on profile inconsistency or absent economic rationale.

What is a DNFBP and why does it matter for real estate buyers?

A DNFBP is a designated non-financial business or profession, and real estate brokers and agents fall into this category, meaning they carry the same core AML reporting obligations as banks and must file STRs with the UAEFIU when warranted.