What is UAE corporate tax in 2026? 9% rate & 0% relief

Many business owners mistakenly believe registering for UAE corporate tax is only necessary if taxable income exceeds the threshold. This misconception can lead to serious compliance issues and costly penalties. In reality, mandatory registration applies to all taxable entities, even those with zero taxable income or qualifying for 0% tax rates. The UAE corporate tax framework, effective since June 2023, introduces tiered rates, exemptions, and relief programs designed to align with international standards while preserving the country’s competitive edge. This guide clarifies definitions, scope, rates, exemptions, compliance requirements, and practical strategies to help you confidently manage your tax obligations and optimize your financial position.

Table of Contents

- Introduction To UAE Corporate Tax

- Scope And Applicability: Who Pays UAE Corporate Tax?

- Corporate Tax Rates And Relief Programs

- Registration, Filing Deadlines, And Compliance Requirements

- Exemptions, Free Zone Treatment, And Special Considerations

- Common Misconceptions About UAE Corporate Tax

- Practical Tax Planning And Compliance Strategies For 2026 And Beyond

- Explore More Resources On Dubai Investments And Business Setup

- Frequently Asked Questions About UAE Corporate Tax

Key takeaways

Introduction to UAE corporate tax

UAE corporate tax is a federal tax on net profits applied from June 1, 2023, under Federal Decree-Law No. 47 of 2022. This legislative framework marks a significant shift in the UAE’s taxation landscape, introducing a modern corporate tax system that balances revenue generation with continued economic competitiveness.

The government designed this tax regime to align the UAE with global tax standards and boost economic sustainability. By implementing tiered rates and targeted exemptions, the framework preserves the UAE’s attractiveness as a business hub while meeting international transparency requirements. The tax applies broadly across mainland and eligible free zone businesses, creating a level playing field for most commercial entities.

Key features of the UAE corporate tax system include:

- Federal application across all emirates, ensuring consistent treatment nationwide

- Effective date of June 1, 2023, for financial years starting on or after that date

- Designed to support the UAE’s long term economic diversification goals

- Preservation of competitiveness through strategic exemptions and relief programs

- Comprehensive coverage of mainland and qualifying free zone entities

You can find detailed information on the UAE Ministry of Finance official corporate tax source, which provides ongoing updates and clarifications on the tax framework.

Scope and applicability: who pays UAE corporate tax?

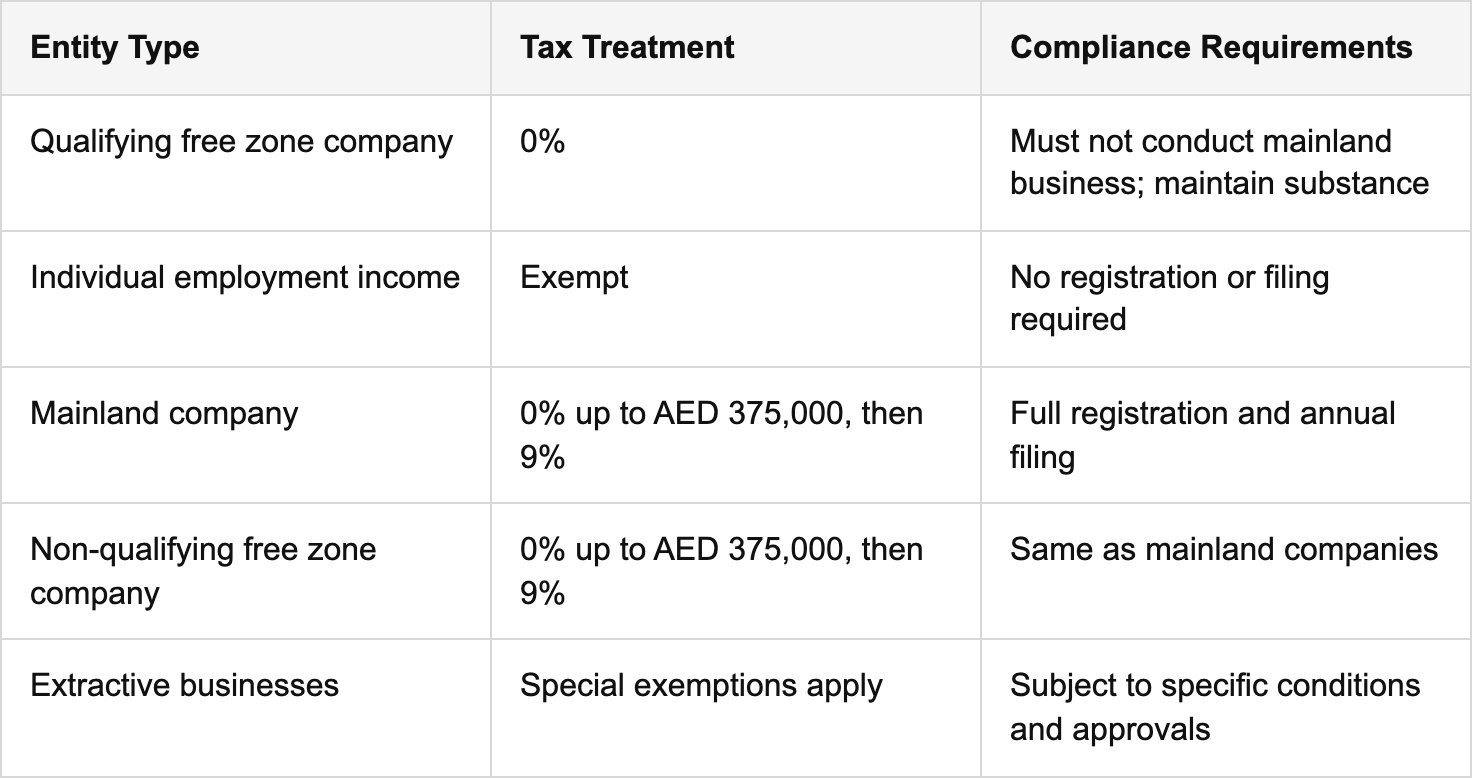

Understanding which entities fall within the scope of UAE corporate tax is crucial for proper compliance. All businesses, including free zone entities with 0% tax rate eligibility, must register for corporate tax with the FTA. This requirement applies regardless of whether you owe tax or qualify for exemptions.

Residency for tax purposes includes two categories: entities established in the UAE under local laws and entities effectively managed and controlled from the UAE. If your business falls into either category, you are considered a UAE tax resident and subject to corporate tax on your worldwide income.

An important distinction exists for individuals. Individuals earning income from employment, bank interest, dividends, or personal investments do not pay UAE corporate tax. This exemption covers salaries, wages, and other employment related compensation, as well as personal investment returns.

Entities subject to UAE corporate tax include:

- All mainland companies holding valid commercial licenses

- Free zone companies that do not meet qualifying conditions for 0% tax

- Foreign companies with a permanent establishment in the UAE

- Non-resident entities earning UAE sourced income

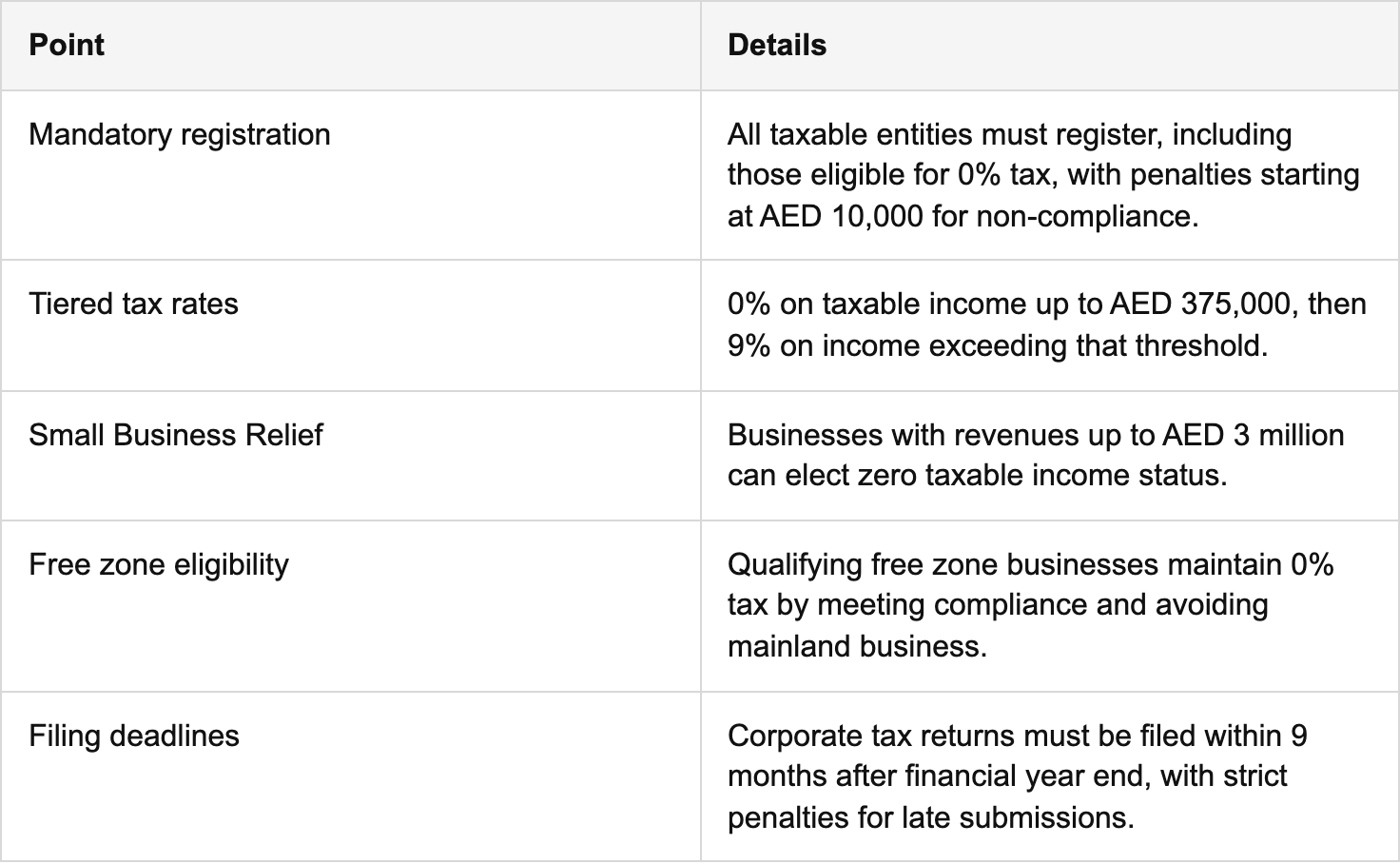

Even if your entity has zero tax liability due to exemptions or losses, registration with the Federal Tax Authority remains mandatory. Failure to register can result in significant penalties, starting at AED 10,000. Understanding how UAE real estate tax applicability intersects with corporate tax can help property investors navigate their obligations more effectively.

For comprehensive details on who must pay corporate tax, consult the official information on UAE corporate tax scope provided by the UAE government.

Corporate tax rates and relief programs

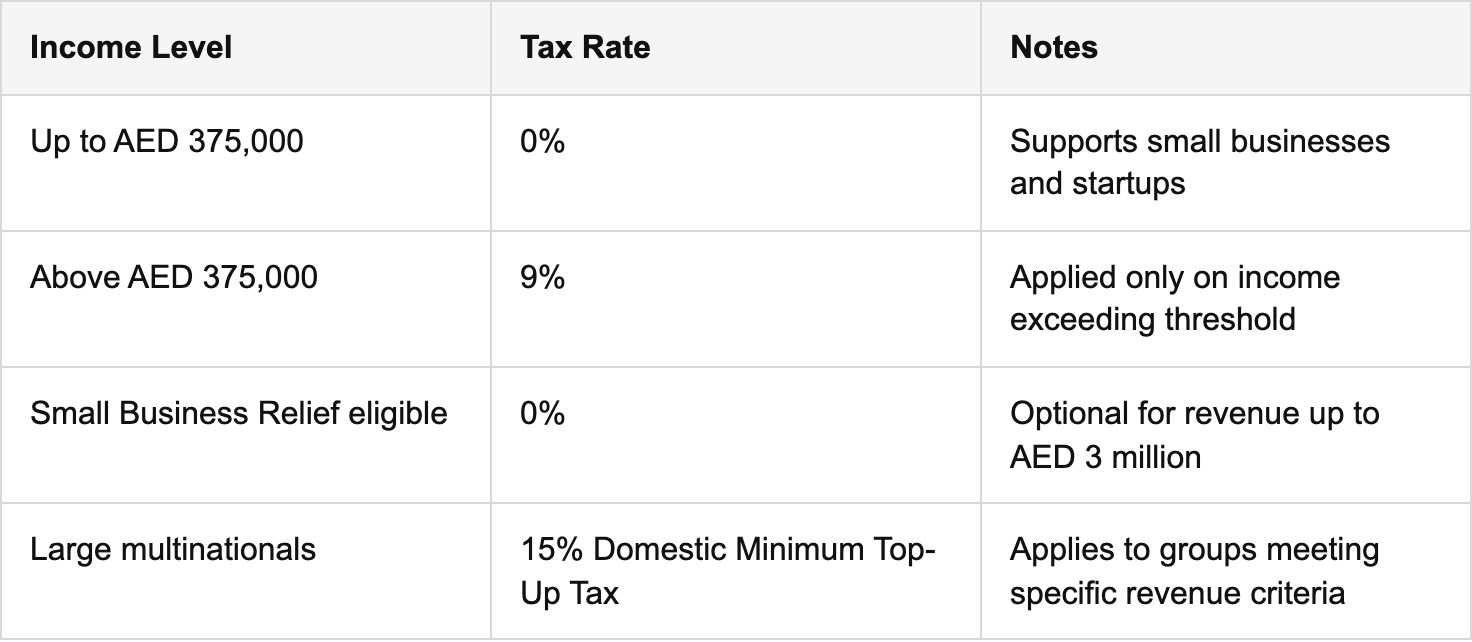

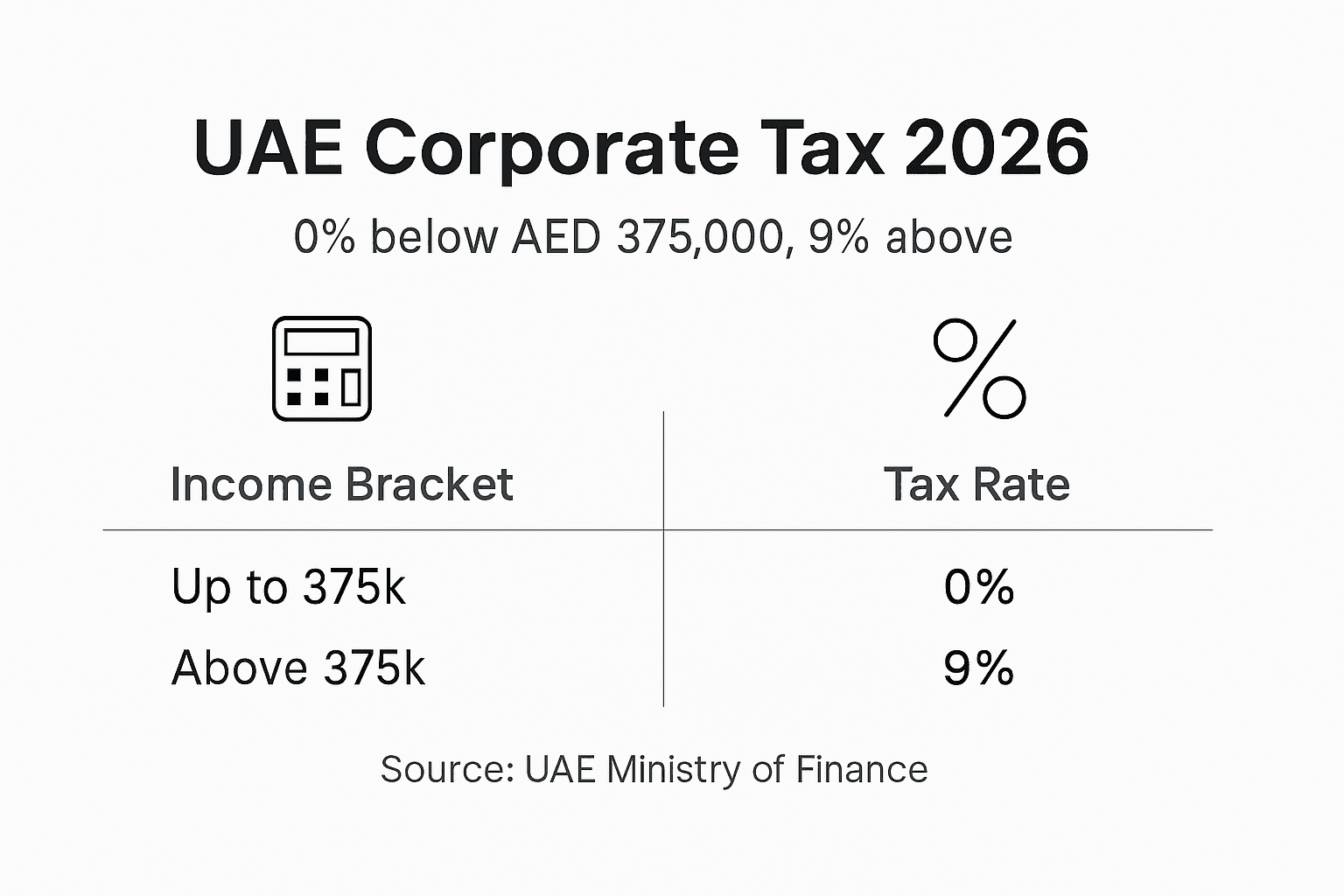

The UAE corporate tax rate is tiered: 0% on taxable income up to AED 375,000 and 9% on income exceeding that threshold. This structure supports smaller businesses and startups while ensuring larger enterprises contribute fairly to national revenues.

The Small Business Relief program allows businesses with revenue up to AED 3 million to elect a zero taxable income status for the tax period. This optional relief simplifies tax compliance for eligible small businesses, though it limits your ability to carry forward losses to future periods. You must carefully evaluate whether this election aligns with your long term tax strategy.

Large multinational groups may face an additional Domestic Minimum Top-Up Tax of 15% if they fall within the scope of the OECD’s Pillar Two framework. This ensures that multinational enterprises pay a minimum effective tax rate on their UAE profits, regardless of other reliefs or exemptions.

Pro Tip: If your business revenue approaches AED 3 million, carefully monitor your financials to determine whether Small Business Relief or standard tax treatment offers better long term benefits. Consider future growth projections and loss carryforward needs before making your election.

Understanding real estate tax rates in Dubai and the benefits of business setup in Dubai can help you optimize your overall tax position across different revenue streams. For specific guidance on relief programs, visit the Small Business Relief details at Federal Tax Authority.

Registration, filing deadlines, and compliance requirements

All businesses, including free zone entities with 0% tax rate eligibility, must register for corporate tax with the FTA. Registration occurs through the EmaraTax portal, the Federal Tax Authority’s digital platform for all tax related submissions and communications.

Your corporate tax return must be filed within 9 months after your financial year end. This deadline applies universally, regardless of your tax liability or exemption status. Missing this deadline triggers automatic penalties and can escalate to more serious consequences if non-compliance continues.

Failure to register or file corporate tax returns on time leads to penalties starting at AED 10,000 and can escalate based on duration and nature of non-compliance. Additional penalties may apply for inaccurate reporting or deliberate misstatements, making timely and accurate compliance essential.

Follow these steps to ensure full compliance:

- Register on EmaraTax within the prescribed timeframe based on your business formation date

- Maintain detailed financial records and supporting documentation for at least 7 years

- Prepare and file your corporate tax return within 9 months of financial year end

- Pay any tax due by the deadline specified in your tax assessment

- Respond promptly to any FTA queries or information requests

- Update your registration details within 20 business days of any material changes

Pro Tip: Set up calendar reminders at least 90 days before your filing deadline to allow adequate time for tax return preparation, review, and submission. This buffer helps you address any unexpected issues without risking late filing penalties.

Proper record retention is critical for audit readiness. You must keep accounting records, supporting documents, and corporate tax returns for at least 7 years from the end of the relevant tax period. These records should include invoices, contracts, financial statements, and documentation supporting all claimed deductions or exemptions.

Understanding legal registration requirements Dubai helps ensure you meet all business setup obligations alongside your tax compliance. For detailed timelines and penalty structures, review the 2026 filing deadlines and penalties guide.

Exemptions, free zone treatment, and special considerations

The UAE corporate tax regime honors existing free zone tax incentives, allowing qualifying free zone businesses to apply 0% tax rates if they meet regulatory compliance and operate without mainland business activity. To qualify, your free zone entity must maintain adequate substance, comply with all relevant regulations, and derive income exclusively from qualifying activities.

Individuals earning income from employment, bank interest, dividends, or personal investments do not pay UAE corporate tax. This exemption clearly separates personal income from business profits, ensuring that salaried employees and individual investors are not caught in the corporate tax net.

Key exemptions and special treatments include:

- Government entities and government controlled entities performing sovereign functions

- Qualifying investment funds meeting specified criteria

- Public benefit organizations approved by the relevant authorities

- Natural resource extraction businesses under certain conditions

- Intra-group transactions that meet transfer pricing and documentation requirements

Qualifying free zone businesses must carefully document their activities to demonstrate eligibility for 0% tax treatment. Any mainland business activity, even a small percentage of revenue, can disqualify the entire entity from preferential treatment. This makes accurate activity tracking and proper invoicing essential.

Understanding Dubai property tax exemptions and Free zone business tax benefits helps you structure your investments and business operations to maximize available tax advantages. For authoritative guidance on exemptions, refer to the official UAE corporate tax exemptions page.

Common misconceptions about UAE corporate tax

All taxable entities, including those with zero taxable income or qualifying for 0% tax, must register with the Federal Tax Authority to comply with the law. This fact contradicts one of the most widespread misconceptions about UAE corporate tax. Many business owners wrongly assume that registration is optional if no tax is due, leading to unintentional non-compliance and avoidable penalties.

Corporate tax does not apply to individual salaries, bank interest, dividends, or personal investment income as these are specifically exempt. Despite this clear exemption, confusion persists among some individuals who worry that their personal earnings might attract corporate tax liability.

Let’s dispel the most common myths:

- Myth: Entities with 0% tax liability don’t need to register. Fact: Registration is mandatory for all taxable entities, regardless of tax rate or liability.

- Myth: Individuals must pay corporate tax on employment income. Fact: Personal employment income, salaries, and wages are completely exempt from corporate tax.

- Myth: Free zone companies are fully exempt and don’t need to file returns. Fact: Free zone companies must register, file annual returns, and prove ongoing qualification for 0% treatment.

- Myth: Small businesses below the AED 375,000 threshold can ignore corporate tax. Fact: All businesses must register, file returns, and maintain records, even if no tax is payable.

- Myth: Corporate tax only applies to large multinational corporations. Fact: The tax applies to all mainland and non-qualifying free zone businesses, regardless of size.

“Understanding the difference between exemption from tax liability and exemption from compliance obligations is critical. Registration and filing are mandatory even when no tax is due, and penalties for non-compliance apply universally.”

These misconceptions often stem from confusion between tax liability and compliance obligations. Even when you owe zero tax, you must still register with the FTA, file annual returns, and maintain proper records. Ignoring these requirements based on incorrect assumptions can result in penalties that far exceed any tax you might eventually owe.

Practical tax planning and compliance strategies for 2026 and beyond

Register early to avoid penalties, even if your projected tax liability is zero. Early registration demonstrates proactive compliance and gives you time to understand reporting requirements before your first filing deadline arrives. The registration process itself can take several weeks, so starting early prevents last minute rushes.

Consider Small Business Relief if your revenue falls below AED 3 million and you don’t expect to carry forward losses. This election simplifies your tax compliance significantly, though it’s not reversible for the elected tax period. Carefully evaluate your multi-year tax position before making this choice.

Follow these strategic steps for optimal tax management:

- Align your financial year end with your business cycle to simplify tax return preparation and reduce accounting costs

- Implement robust accounting systems that track taxable and exempt income separately from day one

- Maintain detailed documentation for all claimed deductions, exemptions, and relief programs

- Prepare transfer pricing documentation if you engage in related party transactions

- Review your free zone qualification status annually to ensure continued eligibility for 0% treatment

- Set up internal controls and approval processes for tax related decisions and filings

- Budget for potential tax liabilities and compliance costs well in advance of filing deadlines

Pro Tip: Conduct a mid-year tax position review to identify any compliance gaps or optimization opportunities before year end. This proactive approach allows you to adjust operations, restructure transactions, or gather missing documentation while there’s still time to act.

Maintain detailed records for at least 7 years to withstand potential audits. Your documentation should include original invoices, contracts, bank statements, financial statements, board minutes, and any correspondence with the FTA. Well organized records dramatically reduce audit risk and associated costs.

Prepare for potential audits by proactively documenting your transfer pricing policies, substance requirements, and basis for claimed exemptions. The FTA may scrutinize related party transactions, free zone qualification, and claimed reliefs more closely, making thorough documentation your best defense.

Exploring business compliance tips and understanding the advantages of Dubai business setup can help you structure your operations for both tax efficiency and long term growth.

Explore more resources on Dubai investments and business setup

Navigating UAE corporate tax is just one aspect of building a successful business in Dubai. Anthony Joseph offers comprehensive resources on Dubai real estate trends 2026 and provides a complete guide to Dubai real estate investment to help you make informed decisions.

Whether you’re establishing a new business, investing in property, or optimizing your existing operations, access to expert guidance makes all the difference. The business blog category features regularly updated insights on market trends, regulatory changes, and strategic opportunities across Dubai’s dynamic business landscape. These resources complement your corporate tax planning by addressing the broader context of operating and investing in the UAE.

Frequently asked questions about UAE corporate tax

Do I need to register for corporate tax if my business has zero taxable income?

Yes, registration is mandatory for all taxable entities, including those with zero taxable income or qualifying for 0% tax rates. The Federal Tax Authority requires registration regardless of your actual tax liability, and penalties for non-compliance start at AED 10,000.

Do individuals pay UAE corporate tax on salaries and personal investments?

No, individuals are exempt from corporate tax on employment income, salaries, bank interest, dividends, and personal investment returns. Corporate tax applies only to business profits earned by legal entities, not to personal income received by individuals.

How do free zone companies maintain their 0% tax eligibility?

Free zone companies must meet strict qualifying conditions including maintaining adequate economic substance, complying fully with free zone regulations, and conducting no business on the UAE mainland. They must also register with the FTA and file annual returns to prove ongoing qualification, even though no tax is due.

What are the filing deadlines and penalties for late submission?

Corporate tax returns must be filed within 9 months after your financial year end. Late registration or filing triggers penalties starting at AED 10,000, with additional penalties for continued non-compliance or inaccurate reporting. Timely filing is essential to avoid these substantial fines.

Can I elect Small Business Relief if my revenue is AED 2.8 million?

Yes, if your revenue is below AED 3 million, you can elect Small Business Relief to report zero taxable income for that tax period. This election simplifies compliance but prevents you from carrying forward losses, so evaluate your multi-year tax position before choosing this option.

What records must I maintain and for how long?

You must keep all accounting records, financial statements, invoices, contracts, and supporting documentation for at least 7 years from the end of the relevant tax period. Proper record retention is mandatory for audit readiness and demonstrating compliance with all claimed deductions and exemptions.