Rent-to-own in Dubai: A complete guide for homebuyers

TL;DR:

- Rent-to-own locks in purchase price but involves non-refundable fees and market risks.

- Contract type (lease-option or lease-purchase) significantly impacts rights, obligations, and financial outcomes.

- Due diligence, legal review, and understanding local regulations are essential before entering Dubai rent-to-own agreements.

Rent-to-own sounds like an ideal middle ground, a way to settle into a home while you work toward ownership. But the reality is more nuanced than most promotions suggest. Many buyers in Dubai enter these agreements without fully understanding the fees they could lose, the obligations they’re taking on, or the regulatory landscape that governs these deals. This guide cuts through that confusion and gives you a clear, practical picture of how rent-to-own actually works in Dubai, what each contract type means for you financially, and how to protect yourself before you sign anything.

Table of Contents

- How does rent-to-own work?

- Key contract structures: Lease-option vs. lease-purchase

- Typical payments and financial risks in Dubai’s rent-to-own deals

- Risks and protections: What to watch out for

- Rent-to-own vs. traditional buying and renting in Dubai

- My perspective on rent-to-own in Dubai’s market

- Ready to explore your options in Dubai real estate?

- Frequently asked questions

Key Takeaways

How does rent-to-own work?

Now that you understand the need for caution, let’s break down how rent-to-own actually works in Dubai.

Rent-to-own, also called lease-to-own, is a contract where you rent a home for a set period and get an option to buy it later at a pre-agreed purchase price. In practical terms, you move in as a tenant, pay monthly rent, and at some point in the future, you have the opportunity to purchase the property at a price locked in from day one. That price lock is one of the most appealing features of the arrangement, especially in a market like Dubai where property values can shift significantly over a two to four year period.

Here is how a typical Dubai rent-to-own contract is structured:

- Rental period: Usually two to five years, during which you occupy the property as a tenant.

- Pre-agreed purchase price: Negotiated and fixed at the start of the contract, regardless of market movements.

- Option fee: An upfront, non-refundable payment that gives you the right to purchase the property at the end of the term.

- Rent credits: A portion of each monthly rent payment, often 10 to 25 percent, that accumulates and is later applied toward your down payment or purchase price.

- Purchase trigger: The point at which you either exercise your option to buy or, depending on the contract type, are obligated to complete the purchase.

Understanding these components is foundational before you explore any specific deal. If you are new to the Dubai rental landscape, reviewing how to rent property in Dubai will give you essential context on tenancy norms and landlord expectations in this market.

It also pays to familiarize yourself with Dubai real estate terms such as freehold, leasehold, RERA (Real Estate Regulatory Agency), and Ejari, all of which directly affect how rent-to-own contracts are registered and enforced here.

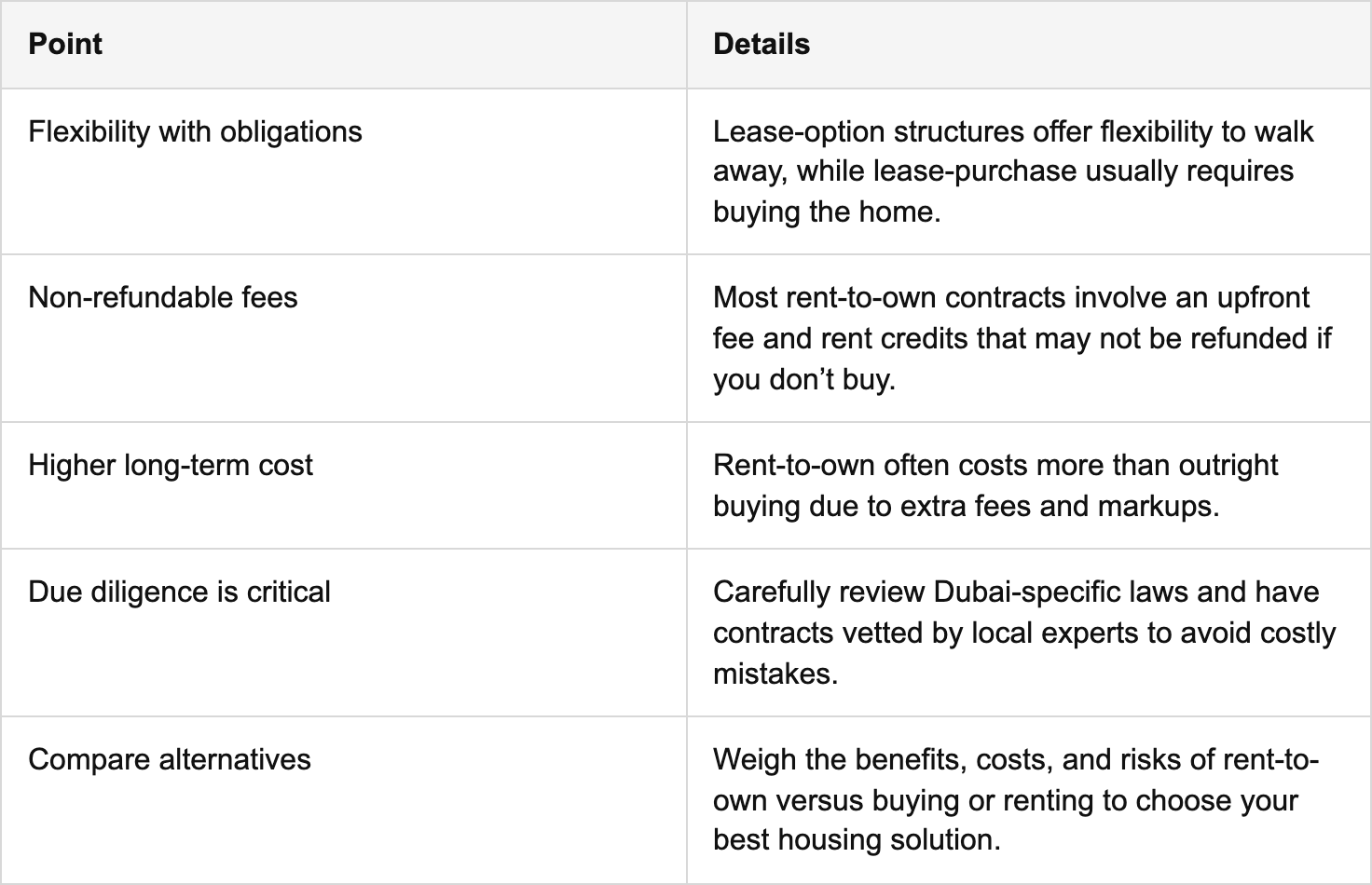

Pro Tip: Always check whether your rent-to-own agreement is a lease-option or a lease-purchase. One gives you a choice; the other locks you into a legal obligation. That difference has major financial and legal implications, which we cover in the next section.

Key contract structures: Lease-option vs. lease-purchase

Once you understand the basic structure, it’s crucial to dig into which type of contract you’re considering.

There are two main contract structures: the lease-option, where you have the right but not the obligation to buy, and the lease-purchase, where you must buy. This distinction sounds simple, but the downstream consequences of each type are dramatically different.

What happens at the end of each contract?

- Lease-option, end of term: You review the market, assess your financial readiness, and choose whether to exercise your purchase option. If you walk away, you forfeit your option fee and any rent credits accumulated.

- Lease-option, mid-term exit: You may leave as a tenant with the typical notice period, but you will lose the option fee.

- Lease-purchase, end of term: You are legally required to complete the purchase. If you cannot secure mortgage financing or the funds to buy, you may face financial penalties, legal action, or forced forfeiture of all payments made.

- Lease-purchase, mid-term exit: Walking away is far more complex and potentially costly, with consequences outlined in the contract that can include breach of contract claims.

For those also considering commercial leasing in Dubai, a similar distinction between obligatory and optional structures applies, and the stakes are even higher at a commercial level.

Pro Tip: Ask your developer or landlord to provide a written breakdown of every scenario in which you could walk away from the contract, and what the precise financial consequences would be in each case. Vague language in a contract almost always works in the seller’s favor, not yours.

Typical payments and financial risks in Dubai’s rent-to-own deals

With contract types in mind, understanding the actual money at stake can help you decide if rent-to-own is right for you.

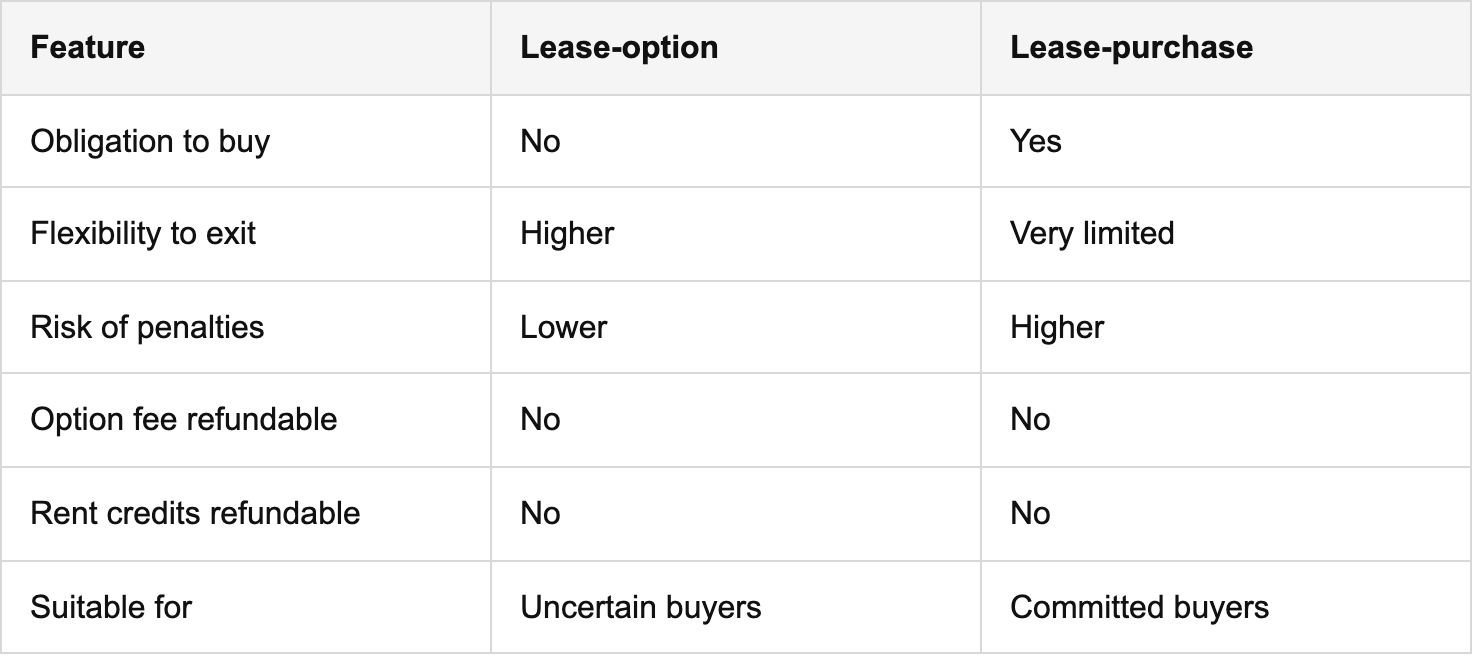

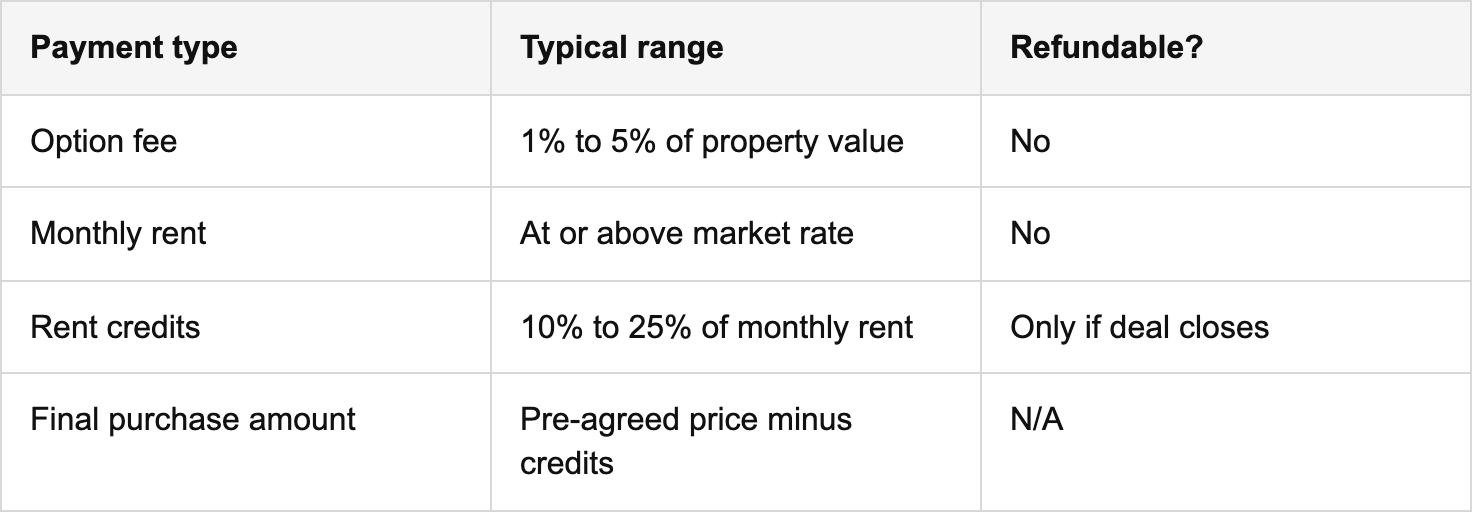

Most rent-to-own deals include an upfront, non-refundable option fee and may also include rent credits, which are portions of monthly payments credited toward the purchase or down payment. In Dubai’s market, the option fee typically ranges from 1 to 5 percent of the property’s agreed value. On a property priced at AED 1,500,000, that means you could pay between AED 15,000 and AED 75,000 upfront, and that money is gone if the deal does not close.

Here is a breakdown of the typical payment components you will encounter:

Beyond the immediate costs, you also carry the risk that property values in Dubai shift during your rental period. If prices drop significantly, you could find yourself committed to a purchase price that is now above market value. If prices rise sharply, you benefit from the locked rate. Neither outcome is guaranteed, which is precisely why due diligence matters.

“If you decide not to purchase, you’ll typically lose money set aside in escrow, rent credits, and usually the option fee as well.” Rocket Mortgage

If you don’t buy by the end of the rent-to-own term, you often lose some or all of the money paid toward the option. This is not a technicality. It is a material financial loss that can run into tens of thousands of dirhams, which is why understanding Dubai rental laws is critical before entering any such agreement.

Dubai’s real estate market is also subject to regulatory updates, currency considerations for expatriates, and banking policies that affect mortgage eligibility. Factors outside your control can make it impossible to qualify for a mortgage by the time your rental period ends, even if your finances look solid today.

Risks and protections: What to watch out for

Recognizing financial risks is the first step, but understanding contract loopholes and protections is key to avoiding major regret.

Contract risks are a significant concern: in some arrangements you can be evicted like a tenant, miss the purchase window, or lose substantial funds if you cannot qualify for financing at the end. Rent-to-own contracts can be complex and frequently fail to result in a completed purchase. The failure rate for these agreements is notably high globally, and Dubai is not immune to this pattern.

Here are the most common risks you need to watch for:

- Mortgage disqualification: If your credit profile, income, or residency status changes during the rental period, you may not qualify for a mortgage when the purchase option arrives, and you will lose all accumulated payments.

- Seller default: In some structures, the seller retains ownership throughout, meaning if they face financial difficulties, the property could be sold or repossessed, leaving you without a home and without your money.

- Property condition issues: As a tenant, you typically bear maintenance responsibilities as specified in the contract, but you don’t own the property. Disputes over condition, liability, and repair costs are common.

- Price lock working against you: In a falling market, you’re locked into a higher price. Walking away is expensive, but completing the purchase at above-market value is worse.

- Regulatory gaps: Consumer protections in Dubai’s rent-to-own space are evolving. RERA provides oversight in traditional rental and sales transactions, but rent-to-own falls into a less clearly defined regulatory category.

“Many rent-to-own deals are never completed, and you may lose the home and the money you have already paid.” Washington Law Help

Regulators often describe rent-to-own as costing more than expected compared with paying cash, due to price markups, fees, and convenience features built into the structure.

Understanding UAE investor rights and risks is essential reading if you want to know how Dubai’s legal framework applies to your situation as a buyer or expatriate tenant.

Pro Tip: Before signing any rent-to-own contract in Dubai, have it reviewed by a licensed real estate broker and a local property lawyer who is familiar with RERA regulations and Ejari registration requirements. The cost of an hour of legal advice is minimal compared to the potential losses.

Rent-to-own vs. traditional buying and renting in Dubai

Now, let’s ground everything in practical terms by comparing rent-to-own to your other main options in Dubai’s market.

Rent-to-own often costs more than paying cash due to price markups, fees, and convenience features. This runs counter to what many people assume. The popular belief is that rent-to-own is a cheaper path to ownership, but the numbers frequently tell a different story.

Rent-to-own tends to make the most strategic sense in a few specific scenarios:

- You are rebuilding your credit score and need two to three years before you can qualify for a UAE mortgage.

- You have relocated recently and want time to assess neighborhoods and lifestyle fit before committing to a purchase.

- You anticipate a significant income increase and want to lock in a purchase price now while building toward a down payment.

- The property you want is not yet available for direct sale because it is under development, and rent-to-own is the developer’s preferred pre-sale structure.

Traditional renting makes more sense if you need maximum flexibility, plan to leave Dubai within two to three years, or are in a strong enough financial position that you do not need the transition period rent-to-own provides. Straight-out purchasing makes the most sense if you have the capital, meet mortgage eligibility criteria, and want to build equity immediately.

Reviewing alternatives to rent-to-own can help you evaluate off-plan investments, standard purchase agreements, and other structures that may better align with your goals and risk tolerance.

My perspective on rent-to-own in Dubai’s market

Here is what I want you to understand from years of working in Dubai real estate: rent-to-own is not a shortcut, and it is rarely as financially favorable as it appears in a developer’s marketing brochure. The contracts are designed to protect the seller first. The non-refundable fees, the above-market rents, and the purchase obligation clauses all serve the interests of the party with more leverage, and that party is almost never the buyer.

What I see frequently is buyers who are genuinely motivated but not quite ready, and who treat rent-to-own as a pressure-free way to “try before they buy.” The problem is that the financial structure punishes hesitation. Every month you pay rent without eventually completing the purchase is money that effectively subsidizes someone else’s asset.

That said, rent-to-own can be a legitimate and strategic tool when used deliberately. The buyers who benefit are those who enter with a clear exit strategy, a firm mortgage pre-qualification timeline, and a legal review of the contract before signing. They treat it not as a lifestyle choice but as a structured financial bridge. If you cannot define exactly what milestone you are working toward during the rental period, you are not ready for a rent-to-own agreement.

Dubai’s real estate market is one of the most dynamic in the world, and the opportunities here are real. But the best outcomes come from making informed decisions with clear eyes, not from chasing arrangements that seem easier than they actually are.

Ready to explore your options in Dubai real estate?

Navigating rent-to-own in Dubai requires more than a basic understanding of contracts. It requires knowledge of local regulations, developer credibility, market timing, and your own financial readiness. That is where having an experienced, trusted advisor makes all the difference.

At anthonyjosephaj.com, Anthony Joseph brings years of award-winning experience in Dubai’s real estate market to help you evaluate every pathway to ownership, including rent-to-own, off-plan investments, and traditional purchases. Whether you are an expatriate buying your first home or an investor building a portfolio, Anthony’s guidance is tailored to your specific situation. Reach out today and get clarity on the contract structures, risks, and opportunities that are relevant to your goals in Dubai.

Frequently asked questions

Can expatriates in Dubai use rent-to-own to buy a home?

Yes, many Dubai rent-to-own programs are open to expatriates, but you should always verify property eligibility in freehold zones and review the specific contract terms for residency-related conditions.

What happens if I can’t get a mortgage at the end of my rent-to-own contract?

You will likely lose your option fee and all accumulated rent credits, and you may face eviction or legal penalties depending on whether your contract is a lease-option or lease-purchase agreement.

Is the option fee in Dubai rent-to-own deals refundable?

No. Option fees are typically non-refundable regardless of whether you choose not to buy or are unable to complete the purchase at the end of the term.

Does rent-to-own cost more than buying a home outright?

It often does. Rent-to-own costs more than paying cash due to price markups, non-refundable fees, above-market rents, and built-in convenience charges that add up significantly over the contract period.

Are rent-to-own homes common in Dubai’s real estate market?

They are available but remain less common than traditional renting or direct purchasing, meaning your selection of eligible properties will be more limited, particularly in established residential communities.