Dubai Equity Release: Unlock Property Value Without Selling

TL;DR:

- Equity release allows Dubai property owners to access capital without selling their assets.

- Eligibility requires a property value of AED 1 million, 60-80% LTV, and certain age and income criteria.

- It is a strategic tool for portfolio growth, provided it is used with clear plans and expert guidance.

You’ve built significant wealth in Dubai real estate, and now you need capital — but selling is the last thing on your mind. That’s a position more Dubai property owners are finding themselves in, and the solution isn’t always obvious. Equity release, a financial mechanism that lets you access the value locked inside your property without transferring ownership, offers a strategic path forward. UAE housing loans extended to age 95 for Emiratis with insurance, with loan-to-value ratios of 60% to 80% and a minimum property threshold of AED 1 million, reveal just how structured and accessible these products have become for qualifying owners.

Table of Contents

- What is equity release and how does it work in Dubai?

- Eligibility: Who qualifies for equity release in Dubai?

- The step-by-step process: How equity release works in practice

- Pros, pitfalls, and strategic uses for Dubai property investors

- Our perspective: How the best investors use equity release in Dubai

- Plan your equity release strategy with expert guidance

- Frequently asked questions

Key Takeaways

What is equity release and how does it work in Dubai?

Equity release refers to any financial arrangement that allows a property owner to access a portion of the capital value tied up in their real estate asset while continuing to own and, in most cases, occupy or manage that property. In simpler terms, you’re borrowing against your asset without giving it up.

In Dubai, equity release typically takes one of these forms:

- Equity release mortgage (remortgage): You refinance an existing property or take a new mortgage against a fully or partially paid-off asset to receive a lump sum. This is the most common approach for high-net-worth individuals (HNWIs) in the UAE.

- Top-up mortgage: If you already have a mortgage, you can request additional borrowing from your lender based on your increased equity, provided your Dubai investor rights and risks are clearly understood and your loan-to-value ratio permits it.

- Cash-out refinance: You replace your existing mortgage with a higher-value loan and receive the difference as cash, which can then be reinvested or deployed strategically.

- Lifetime mortgage equivalent: Though less formalized in the UAE than in markets like the UK, some senior Emirati borrowers can access long-term arrangements where the loan is secured against the property and repaid when the asset is sold or transferred.

The mechanics depend heavily on which bank or lender you approach, the nature of your property (freehold or leasehold), and your residency status. UAE banks operate under Central Bank guidelines, which set clear parameters around loan amounts, tenures, and qualifying criteria. Property must be fully registered with the relevant land department, and its valuation must be conducted by a Central Bank-approved evaluator.

Key insight: Equity release in Dubai is not a single product — it is a category of financial instruments. Choosing the right structure for your situation requires matching your liquidity goals, risk profile, and reinvestment plan to the appropriate product.

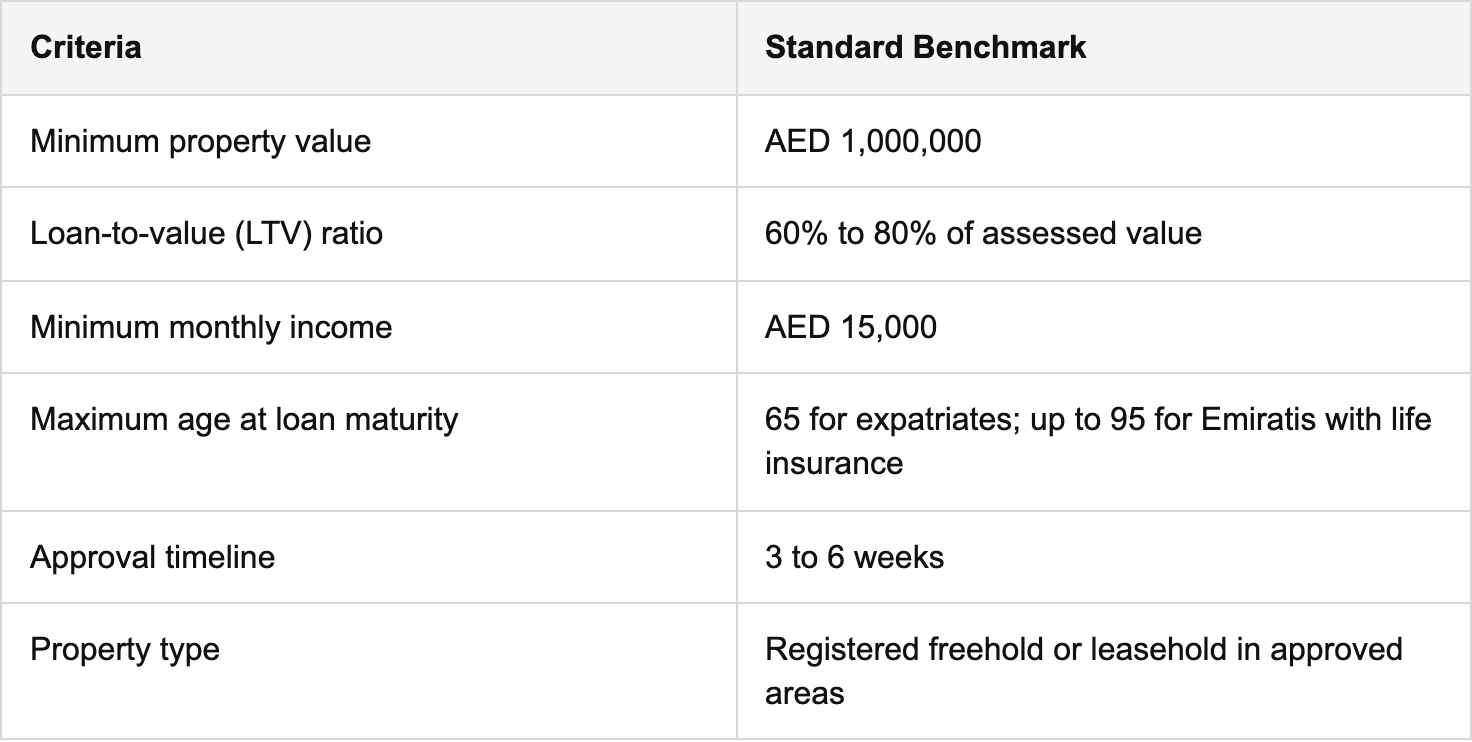

Standard benchmarks you’ll encounter include LTV ratios of 60% to 80%, a minimum property value of AED 1 million, and a minimum verified monthly income of AED 15,000. The entire process from initial application to fund receipt typically runs 3 to 6 weeks.

Eligibility: Who qualifies for equity release in Dubai?

Understanding how equity release works, it’s critical to see if you, given your profile and assets, meet Dubai’s eligibility benchmarks for these products.

Eligibility criteria in the UAE are specific and non-negotiable at most institutions. Here’s a breakdown of the core requirements:

These benchmarks come directly from published lender requirements. Eligibility benchmarks for UAE products confirm that Emiratis can access housing loans with maturities stretching to age 95 when life insurance is attached, making equity release a genuinely long-term planning tool for senior citizens in this category. Expatriates, by contrast, face tighter age thresholds, typically capped at 65 years of age at the time the loan matures.

For high-net-worth applicants, the income threshold of AED 15,000 per month is rarely a barrier. The more relevant variable is the LTV ceiling. If your property is valued at AED 5 million, you can release between AED 3 million and AED 4 million, depending on the lender’s assessment and your existing liabilities.

Pro Tip: Before approaching a bank, obtain an independent property valuation from a Central Bank-approved valuator. Knowing your number before the bank does gives you a stronger negotiating position and prevents being surprised by a lower-than-expected assessed value.

Consider three profile types that commonly benefit from equity release in Dubai:

- The portfolio builder: An investor who owns a fully paid-off villa in Emirates Hills and wants to fund the acquisition of two additional off-plan units without liquidating the primary asset.

- The business owner: A business proprietor who owns high-value Dubai real estate and needs liquidity to expand operations or fund a new venture without touching operational capital.

- The senior Emirati investor: A property owner with long-held assets who wants to access capital for family needs or wealth redistribution while retaining the family home within the estate.

Each case calls for a different structure, but all three can be served by equity release when the underlying criteria are met.

The step-by-step process: How equity release works in practice

Having confirmed you’re eligible, here’s what to expect if you decide to proceed, from paperwork to payout.

-

Pre-application preparation: Gather your key documents — Emirates ID or passport, proof of income (salary certificates or audited financial statements for business owners), property title deed, existing mortgage statement if applicable, and recent utility bills for address verification.

-

Engage a lender or mortgage broker: Approach your existing bank or use a UAE-licensed mortgage broker to compare products across multiple institutions. Rates, LTV ceilings, and fees vary significantly between lenders, and the broker’s market knowledge can save you both time and money.

-

Independent property valuation: The lender commissions an official property valuation through a Central Bank-approved firm. This assessment determines the maximum loan amount you can access. Do not skip obtaining your own estimate beforehand.

-

Loan-to-value negotiation: Once the valuation is received, the lender presents a loan offer based on their LTV policy. Experienced borrowers negotiate at this stage, particularly if the property is in a prime location with strong market demand. Understanding Dubai real estate workflows helps you recognize what is and isn’t negotiable.

-

Compliance and credit checks: The bank conducts full credit bureau checks, verifies your liabilities, and assesses your debt-to-burden ratio. The UAE Central Bank caps total monthly debt obligations at 50% of gross income for most borrowers.

-

Life insurance requirement: For longer loan tenures, particularly those extending toward retirement age, most lenders require you to take out a decreasing term life insurance policy. For Emiratis accessing the age 95 product, this is mandatory.

-

Final approval and offer letter: Once all checks pass, the lender issues a formal offer letter. Review this carefully, particularly the interest rate (fixed or variable), early settlement penalties, and any conditions attached.

-

Fund disbursal: Upon signing and completing the legal documentation, funds are released. The process typically takes 3 to 6 weeks from initial application to receipt of funds, though well-prepared applicants with clean documentation often complete it closer to the three-week mark.

Statistic to note: Dubai’s real estate market recorded over AED 760 billion in total transactions in 2024, a reflection of the depth and liquidity that makes property-backed financing in this market particularly attractive for lenders and borrowers alike.

Pro Tip: Submit your documentation in a single, complete package rather than in stages. Incomplete submissions are the single biggest cause of delays in UAE bank processing times. A well-organized application signals professionalism and can accelerate your approval timeline noticeably.

Pros, pitfalls, and strategic uses for Dubai property investors

Now you’ve seen the mechanics and workflow. Let’s evaluate if equity release is strategically sound for your Dubai portfolio and where to proceed with caution.

Direct sale vs. equity release: A strategic comparison

The strategic advantages of equity release for Dubai HNWIs are compelling when conditions align:

- Portfolio diversification without liquidation: You retain a performing asset that continues generating rental yield while deploying released capital into a new investment class or geography.

- Interest rate arbitrage: If the return on your reinvested capital exceeds the interest rate on your equity release loan, you create net positive leverage, a core principle in sophisticated real estate wealth management.

- Tax efficiency: The UAE has no capital gains tax, which reduces one traditional objection to equity release in other markets. Released funds are not a taxable event.

- Estate and succession planning: For families, retaining property ownership while accessing capital allows more flexible intergenerational wealth structuring.

However, there are real risks you must acknowledge:

- Interest accumulation: Equity release loans carry ongoing interest costs. If your released capital is not deployed productively, the loan erodes rather than builds your net worth.

- Market downturns: If Dubai property values decline significantly, the LTV ratio can shift against you, creating a situation where your outstanding loan approaches or exceeds the asset’s current value.

- Long-term commitment: These are not short-term instruments. Entering an equity release arrangement without a clear five-to-ten year financial plan is a common mistake.

Strategic principle: Equity release is a tool for acceleration, not rescue. If you are releasing equity because you are financially stressed, it is almost always the wrong solution. If you are releasing equity because you have identified a high-confidence reinvestment opportunity, it can be genuinely transformative.

For investors who want to understand the full strategic landscape before committing, reviewing data-driven Dubai real estate strategy analysis is an essential starting point. LTV ceilings of 60% to 80% mean you always retain meaningful equity in your property, which is itself a form of risk mitigation built into the system.

Our perspective: How the best investors use equity release in Dubai

Most conversations about equity release in Dubai focus on the mechanics and the eligibility boxes to check. That is useful, but it misses the more important question: when should you actually use it?

The conventional wisdom says equity release is for cash-strapped property owners who want to access value without selling. That framing is limiting, and in the UAE context, it’s often wrong. The investors we see using equity release most effectively are not doing so out of necessity. They are doing it as an offensive financial move during a window when opportunities are priced favorably.

Dubai’s real estate market moves in cycles. Staying current with Dubai market trends reveals something most investors overlook: the optimal moment to release equity from an existing property is before a market surge, not after prices have already risen and borrowing against inflated assets becomes more expensive in real terms.

Here’s what we observe among genuinely strategic Dubai investors. They treat their existing portfolio not as a static collection of assets, but as a dynamic source of capital efficiency. When a strong off-plan opportunity appears, or when a distressed sale is available at a meaningful discount, they don’t wait to sell an existing asset. They release equity and move fast. Speed is a competitive advantage in Dubai’s market, and equity release — when pre-arranged through a lender relationship — can be the mechanism that enables it.

The one discipline we’d insist on: never enter an equity release arrangement without a defined exit strategy for the released funds. This is where many well-intentioned investors make mistakes. The loan is real, the interest is real, and unless the capital is working harder than the borrowing cost, you are simply paying to hold liquidity. That is not strategy. That is expensive indecision.

The investors who truly benefit from equity release in Dubai are those who use it as a bridge to a specific, time-sensitive opportunity, with a clear repayment plan anchored in either rental income, asset appreciation, or an exit event.

Plan your equity release strategy with expert guidance

Equity release in Dubai is a high-value tool, but it requires precise execution to deliver the results you’re aiming for. The difference between a well-structured arrangement and a costly misstep often comes down to the quality of guidance you have at the planning stage.

Anthony Joseph and his team specialize in helping high-net-worth investors navigate Dubai’s real estate landscape with clarity and confidence. Whether you’re assessing your current portfolio’s equity potential, identifying reinvestment opportunities, or simply need a second opinion before approaching a lender, expert-led guidance is the foundation of a sound strategy. Explore bespoke equity release solutions tailored to your specific financial goals and property profile, and take your next strategic step with a trusted specialist who understands what Dubai’s market demands in 2026.

Frequently asked questions

How much equity can I release from my Dubai property?

You can typically release between 60% and 80% of your property’s assessed value, depending on the lender’s policies, your income profile, and existing liabilities.

What is the minimum property value required for equity release?

Most UAE banks require the property to be valued at a minimum of AED 1 million to qualify for an equity release product, though some premium lenders set their floor higher.

How long does the equity release process take in Dubai?

The process generally takes 3 to 6 weeks from initial application to fund disbursal, with well-prepared applicants often completing toward the shorter end of that range.

Can expatriates access equity release in Dubai?

Many UAE banks offer equity release products to expatriates who meet strict income, LTV, and age criteria, though the maximum loan maturity age is generally lower for expats than for Emirati nationals.

Is equity release a good idea for portfolio diversification?

For high-net-worth investors with a clear reinvestment opportunity, equity release can provide meaningful liquidity while preserving ownership of a performing asset, making it a strategically sound tool when used with discipline.